A lot of us digital nomads, serial expats, and others in the location-independent crowd can live and work from anywhere because we run our own independent businesses.

But no matter if you’re an indie maker, consultant, web developer, or mindfulness coach you’re likely to have run into the nightmare which is business banking for small and/or location-independent businesses.

You’ve probably already learned that most business banks accounts:

- Are ridiculously hard (if even possible) to open

- Charge you an arm and a leg in fees

- Screw you over on the exchange rate when converting currencies

While I’ve covered most of the cheap and easy to open personal bank accounts in major countries worldwide, I have yet to do the same for business bank accounts that can be opened online—from anywhere. Until now.

Table of Contents ↺

I want to be a bit more liberal with the “banking” term this time around. Most business accounts that are low cost and easy to open remotely for most people are offered by fintech companies (a.k.a. neo or challenger banks), often without full banking licenses.

In practice, this distinction isn’t always that important, since these companies are still regulated and your funds are typically held in segregated accounts with solid partner banks.

In this article, I have listed all the banks and bank-like services relevant for anyone running a small, international business. Since many of us run companies registered in a country where we’re not (full time) resident, I’ve focused on those that are easy to open and manage remotely, even if you’re not a legal resident in the country of the bank.

While some of these business bank accounts are available no matter where your company is registered, some require that you have a company in their jurisdiction. For the latter, I’ve focused on popular location-independent business jurisdictions, such as the US, UK, Hong Kong, and the EU (including Estonia).

International

Let’s start with the international category, which I define as companies offering banking services with local bank details in several important jurisdictions.

These allow you to receive payments from customers across the world, as if you had a real bank account in their country. Some (like Wise) also help you save loads of money on currency conversion costs.

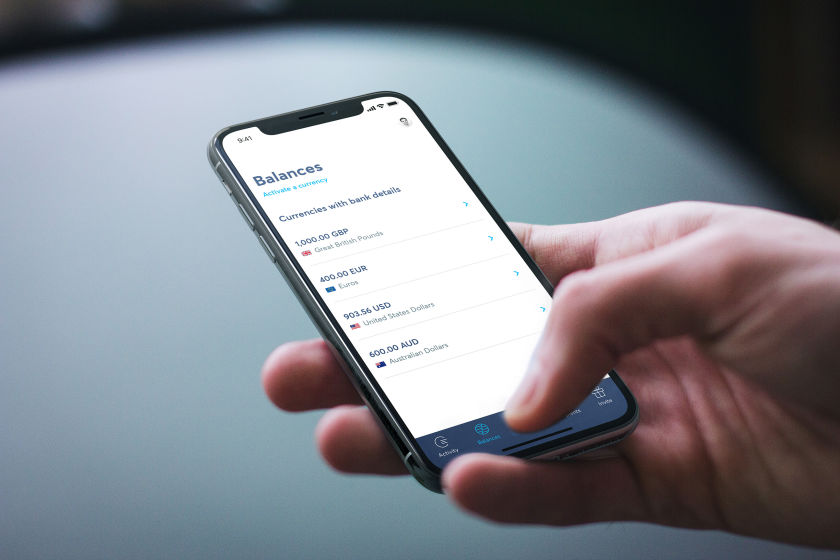

Wise Business

I think Wise’s “borderless” business account product is one of the best things that happened to us digital nomads and location-independent entrepreneurs—at least when it comes to simplifying our business finances and saving on fees. I’ve been using it for every single one of my companies in recent years.

In case you haven’t already heard about it, let me briefly explain what it is:

Wise now lets you open business (and personal) bank-like accounts in the following jurisdictions:

-

United States—with full ACH and wire details

-

United Kingdom—with local account number and sort code

-

the Eurozone (Germany or Belgium) – with a full IBAN

-

Hungary—with local account number

-

Australia—with local account number and BSB code

-

New Zealand—with a local account number

-

Canada— with local account number, transit number, and institution number

-

Turkey— with your own Bank name and IBAN

-

Singapore—local account number with DBS Bank

-

Romania – IBAN is available for residents of Romania and the UK.

Romania – IBAN is available for residents of Romania and the UK.

All of these accounts are in the name of your company—and unlike Payoneer you can accept any type of (legal or non-restricted) payments and outgoing transfers also come from your company name.

You can also open currency wallets in more than 40 other currencies, although you don’t get unique bank details for these (yet).

Not only that—but you also get a free debit card linked to your account. There are no fees for spending in the currencies you hold in your account, and for any other currencies you get Wise’s low exchange fees (often around 0.5% markup) on top of the true interbank/mid-market rate!

If you use Stripe to sell products or services online in different currencies (e.g. EUR, USD, GBP, AUD, and NZD) you can link those accounts to Stripe and save the 2% currency exchange fee they normally charge.

The same goes if you have income from e.g. Amazon or other sources in different countries and currencies. They are a member of the Amazon payment service provider program, which means that you can now use Wise to receive any sales earnings in over 50 different currencies, making it great for ecommerce businesses, dropshippers, and wholesale companies. Read here for more info about Wise for ecommerce businesses.

Wise Business at a glance

Highlights

-

Open for both freelancers and businesses registered in most of the world

Open for both freelancers and businesses registered in most of the world

. Exceptions listed here.

. Exceptions listed here.

-

Supports 40+ currencies and transfers to suppliers in 70+ countries, with unique bank details in the Eurozone (Belgium

), Hungary , UK , USA , Australia , New Zealand , Canada , Turkey , and Singapore . Romanian IBANs are available for UK and Romanian residents.

), Hungary , UK , USA , Australia , New Zealand , Canada , Turkey , and Singapore . Romanian IBANs are available for UK and Romanian residents.

-

Comes with free debit card for business expenses (available in the UK, EU/EEA, Switzerland, Australia, New Zealand, Canada, Japan, and Singapore at the moment).

-

Low fees

for currency exchange and outbound money transfers. No fees for sending to other Wise users.

for currency exchange and outbound money transfers. No fees for sending to other Wise users.

-

£200 of free cash withdraws

per month. (But who withdraws cash from their business account anyway?)

per month. (But who withdraws cash from their business account anyway?)

-

Great for e-residents

using Xolo to manage their business—or anyone else using Xero for accounting—thanks to direct integrations.

using Xolo to manage their business—or anyone else using Xero for accounting—thanks to direct integrations.

-

Available both on web

, iOS

, iOS  , and Android

, and Android  .

.

-

USD, EUR, GBP, and AUD accounts supports direct debit, other currencies will follow.

-

Regulated by the FCA (Financial Conduct Authority)

in the UK as an e-money provider.

in the UK as an e-money provider.

-

Competitive interest rate on your deposits in USD, EUR, GBP. As of September 2025 you earn up to 3.9% depending on the currency.

Things to note

-

The online card spending limit of £45,000/mo may not be enough for everyone. Bank transfers are not limited, though.

The online card spending limit of £45,000/mo may not be enough for everyone. Bank transfers are not limited, though.

-

There's a one-time business account opening fee in some countries (e.g. $31 in the US, ~€50 in Europe).

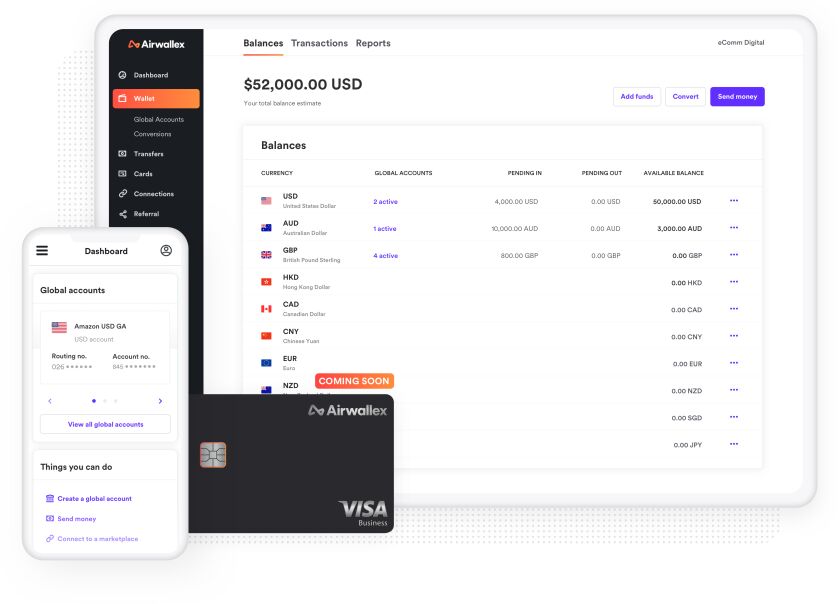

Airwallex

Airwallex is an Australian origin fintech offering business banking services for companies since 2015. Although not yet quite as well-known as Wise, they definitely have a solid, competitive product which they have improved and expanded significantly in recent years.

They offer their services to companies registered in more than 180 different jurisdictions, including the likes of Australia, China, Estonia, Germany, Hong Kong, Luxembourg, Malta, Malaysia, New Zealand, Seychelles, UAE, the UK, the US, BVI, and many more.

Airwallex offers multi-currency accounts across 20+ currencies with local bank details in 11+ countries. Zero FX margin when balance exists in the 10 main direct-billing currencies. Airwallex waives these fees entirely. In case of insufficient balance, the auto-conversions are executed at Visa daily rate + ~1% markup.

You can receive payments directly from Amazon, eBay, Shopify, and PayPal. They even have WeChat pay that allows businesses to receive money from Chinese consumers easily, as well as multiple other local payment methods from around the world, such as Kakao Pay (Korea), GrabPay (Singapore) and many more. They also have a mobile app supported both on Android & iOS.

Just like Wise, they offer an integration with Xero for a better accounting experience. They will sync your records frequently, and batch payments are also supported for more convenience.

Every employee can have their own virtual card and logins to keep better track of spendings. Physical cards and Apple Pay & Google Pay are currently available in Australia, New Zealand, Hong Kong, Singapore, the United Kingdom, the United States, Canada, and EU/EEA customers.

Special offer:

Get $500 bonus for the first $15K spend within 90 days for US-based companies

Get 10% cashback on the first $1,000 foreign currency transactions within 30 days for companies in most of continental Europe

Airwallex at a glance

Highlights

-

Payments possible in more than 60 currencies including USD, GBP, EUR, AUD, CNY, HKD, and CAD

-

Can have 11+ global accounts in 20+ currencies (including, AUD, CAD, EUR, SGD, HKD, CNY, IDR, ILS, MXN, NZD, PHP, SGD, GBP, USD, AED)

-

Physical cards available for customers in more than 50 countries

-

Zero FX margin when holding the balance in your account in 10 direct-billing currencies

-

Direct payments from Amazon, eBay, Shopify, PayPal, and WeChat

-

No deposit limits to receive money in your account

-

Integrated with Xero

-

Separate cards and logins for employees

-

Mobile app for Android & iOS

Things to note

-

There may be an extra FX markup on the weekend or other days when FX markets are closed

-

While virtual company cards are completely free, physical employee cards may cost extra. There are regional differences, but in UK/EU they allow 5 free employee card, and over that there's £5 fee per card per month

Payoneer

Payoneer has been a pioneer in the international payments industry since they launched their USD receiving accounts back in 2011. For many people (e.g. if you don’t qualify for a Wise account) it’s still the only option for getting US account details or to get paid from many online marketplaces.

Note that you can only receive funds from companies (e.g. marketplaces such as Amazon or UpWork), not from private individuals—so you can’t use Payoneer to get paid from non-corporate clients.

While Payoneer has proved super useful to the otherwise unbanked—they also charge extremely high fees, so it’s best to avoid them if you have other options available to you.

Receiving USD costs 1% of the transaction, other currencies free. Spending money with the Payoneer debit card (which costs $30/year) costs 3.5% if used outside the country of issue (typically US or UK) or if used in a different currency. ATM fees are high, exchange rates unfavorable (typically 2-3% markup), and even withdrawing money to a normal bank account costs 2%.

Payoneer at a glance

Highlights

-

One of the first bank-like products providing access to receiving-accounts in the world’s largest economies to people resident anywhere.

-

Nearly anyone can open an account.

-

10 global currency accounts available

Things to note

-

Fees are a bit high for certain transactions.

-

Not meant to replace your bank account, but to supplement it. E.g. outbound transfers do not come from your business name, and not all inbound transfers are accepted.

-

The online card spending limit of $15,000/day may not be enough for every business. Though, bank transfers have a much higher limit of $100,000 USD/EUR/GBP.

United States

Let’s move on to the land of the free. While you can still open a business account as a non-resident in several large US banks—especially if you show up in person and agree to a large initial deposit—that’s impractical for most of us.

Options such as Wise above is still good enough for most foreign companies, but if you have a US entity (even as a non-resident foreigner) read on to learn how you easily can open a US business account remotely, for free.

Tip: If you need a proper US account for a primarily non-US business, it’s cheap and pretty straightforward to register a non-resident LLC in many US states, and it shouldn’t have any tax consequences. I’d recommend New Mexico and Wyoming for most purposes (especially if you value privacy), or Delaware in the case you have ambitions of raising money or selling the business down the line.

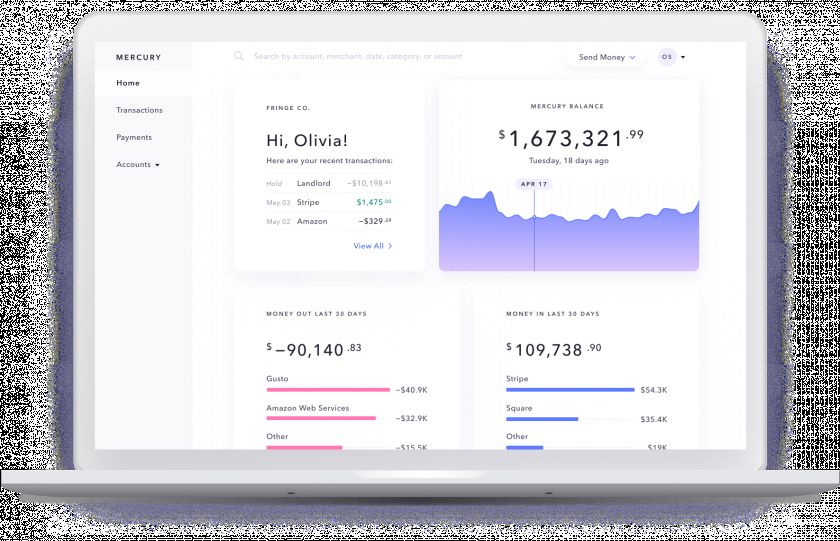

Mercury

I was a bit surprised that Mercury didn’t initially receive more attention in the location-independent business community since after their launch in April 2019.

The original version of this article (from December 2019) was likely the first article targeted at digital nomads, PTs, and other location-independent people featuring them.

However, by now they are quite well known.

If you are a non-US resident with a US business (e.g. LLC or corporation) who needs to an easy-to-use business account, with low fees, that you can open remotely—this is the one to get.

Mercury recently revamped its fee structure, eliminating charges for both domestic and international wire transfers altogether.

On the flip side, they now charge a 1% conversion fee on non-USD international wires, and a 3% currency conversion fee on non-USD card transactions. While much lower than most US-based banks, if you do a lot of foreign transactions you may want to pair it with for example a Wise Business account to save even more.

That said, it’s now the only thing they charge for, so the overall package is still very attractive. Additionally, for those processing over $200K/month, they offer customized rates upon contact.

Everything else, from ACH transfers to ATM withdrawals, remain completely fee-free. However, they do add 3% conversion fee for non-USD ATM withdrawals.

Mercury at a glance

Highlights

-

No wire transfer fees, ATM withdrawal fees, account opening fees or overdraft fees—just a 1% foreign exchange fee for wires and 3% for card usage in non-USD currencies

-

Open for companies registered in the US, including LLCs and corporations with foreign resident managers/owners

-

Real US bank account with associated debit card

-

Relatively high interest rates

-

Can be used with US PayPal and Stripe accounts

-

Powerful API so if you're technical you can automate a lot of your banking

Things to note

-

Outgoing transfers are not made in the name of the business, but rather Mercury (business name can still be added to message)

-

If asked it's better to state that you'll do business with US companies (not necessarily exclusively), as they may otherwise not approve your account

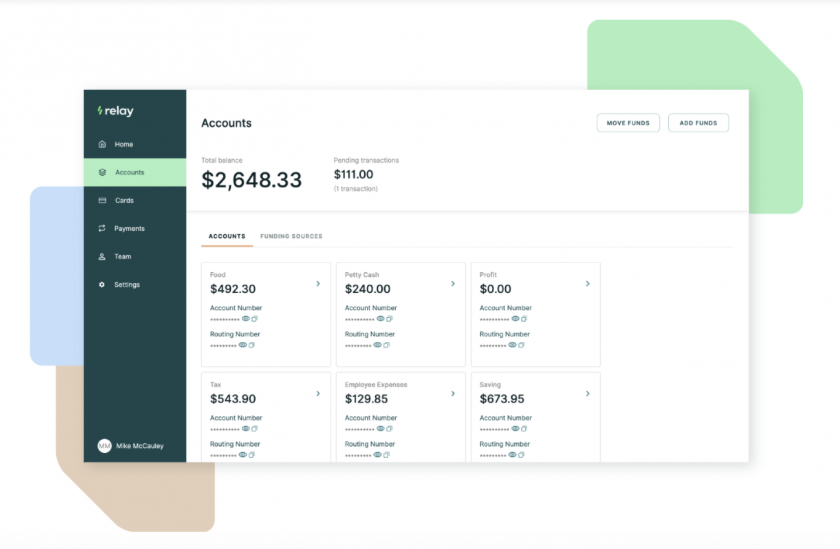

Relay

Another great remote business banking platform for the US is Relay. And this recommendation comes from our very own Nomad Gate readers.

The standard ACH transfers are free unlimited. They charge for wire transfers—$8 for domestic and $5 for international (in main currencies). The wires with the paid Grow and Scale plans become cheaper per wire.

It has other great business banking and budget management features such as the ability to issue debit cards to your team, set spending limits, track expenses, as well as integrate accounting tools such as Xero and Quickbooks.

Relay at a glance

Highlights

-

Low fees for both domestic and international wire transfers

-

Great reviews for its customer support team

-

Supports US corporations, LLCs, sole proprietors, and freelancers in over 200 countries

-

No minimum balances, low currency exchange fees (1%), and unlimited transactions

-

Interest payments for savings account , starting from 1.03% APY on free plan and cash back on credit cards (from 1% on free plan)

Things to note

-

Doesn't accept restricted industries such as crypto, privately owned ATMs, money services, unlawful internet gambling, or cannabis sales.

Europe

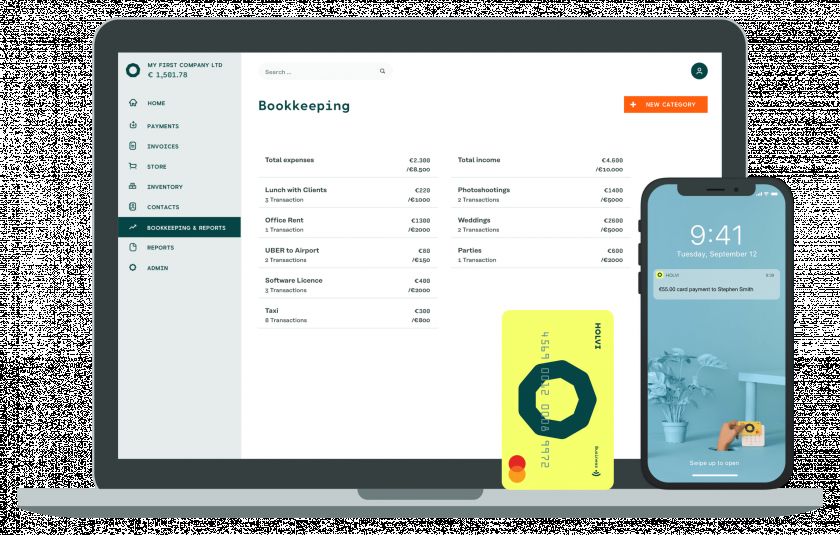

Holvi

Holvi is a Finnish ![]() challenger bank—technically a payment institution as they don’t have a full banking license. Regulated by both the Finnish and German financial supervisory authorities, giving you the choice of either a Finnish or German IBAN.

challenger bank—technically a payment institution as they don’t have a full banking license. Regulated by both the Finnish and German financial supervisory authorities, giving you the choice of either a Finnish or German IBAN.

Their offering is a solid combination of business banking features, simple bookkeeping and invoicing features (from the €9/mo Holvi Lite plan and up).

You get a bright yellow Mastercard debit card and unlimited free SEPA transfers (if you’re based in the Eurozone). Beyond SEPA, Holvi supports SWIFT transfers at a rate of €6 per transfer, plus FX fees.

Holvi at a glance

Highlights

-

Provides Finnish or German IBAN

-

Open for freelancers and businesses registered in several EU countries

-

Very popular for German, Finnish, and Austrian businesses; Unlimited free domestic transfers

-

Real debit card, not prepaid, meaning better acceptance

-

Pricing tiers from €9/month (Lite) to higher tiers (Pro, Zen, Flex) offering more features

-

Accounts include simple invoicing and accounting tools

-

Regulated by the Finnish Financial Supervisory Authority (FIN-FSA) as a payment institution

Things to note

-

No longer available for UK customers

-

Use in foreign currencies could be cheaper (2% markup over the Mastercard rate)

-

ATM withdrawals have another 2% surcharge (regardless of currency)

N26 Business

N26 is a German ![]() neobank who’s main claim-to-fame is one of the best personal bank accounts for travelers. Their business product is almost identical—which is both good and bad.

neobank who’s main claim-to-fame is one of the best personal bank accounts for travelers. Their business product is almost identical—which is both good and bad.

On the plus side you get a fantastic mobile and web app, some of the lowest fees available in Europe, and some pretty handy budgeting features.

You also get unlimited free SEPA transfers. For non-SEPA transfers, you can use Wise (see above).

One added bonus for the business account (compared to the personal one) is the addition of 0.1% cashback on all your purchases (or 0.5% for their metal card).

You can also get included travel insurance and zero ATM withdrawal fees in foreign currencies by opting for the Business Go (€9.90/mo) and Business Metal account (€16.90/mo). You’ll also get travel, mobility, baggage delay, personal liability insurance and exclusively for Metal plan also purchase protection and phone insurance.

The drawback of the N26 account is that it’s only available for freelancers and self-employed. You can’t use it for an incorporated business. It’s also pretty weak when it comes to bookkeeping and invoicing features (they are pretty much absent).

N26 Business at a glance

Highlights

-

Provides fully insured bank account with German IBAN

-

Open to freelancers (not corporations) across all the EEA countries where N26 operates

-

You earn 0.1% (or 0.5%) cashback on all card transactions

-

No/very low fees

-

Good travel insurance for premium plans

-

Often special deals and discounts with partners (former and current examples include Hotels.com, GetYourGuide, Booking.com, Lime, YOOX, Taxfix, etc.)

Things to note

-

You can't have two N26 accounts in the EU, so you have to choose between either a personal or freelancer account. My recommendation would be to use N26 for your personal banking, and use Wise or Holvi for your business activity.

-

Lack of useful accounting and invoicing features

-

Monthly card spending limits of €20,000, daily €5,000 for in-store or online payments

Monese Business

Monese is (like N26) perhaps best known for their personal banking product, but their business account is also great!

Together with Tide (below) and Wise it’s one of the few banking options for non-UK residents with a UK registered company.

It does come with a small monthly fee (£9.95), but the included services are more than worth it.

You’ll get six free ATM withdrawals per month, only 0.5% currency markup on spending and international transfers, and free incoming and outgoing bank transfers, including direct debits. International transfers to non-Monese accounts incur a 0.5% fee, with a £2 minimum charge.

Monese Business at a glance

Highlights

-

Unlike most UK banks, they accept UK companies with foreign directors/owners living in the EU/EEA

-

For £9.95 you get a user-friendly business account, with no/very low transaction fees

-

You will get local GBP account details

-

It also includes a personal free (Simple) Monese account

Things to note

-

To open a business account, you'll have to open a personal Monese account first (meaning you'll need to be resident in the UK or EU/EEA)—then you set up the business account with a few taps inside the app

-

Somewhat low limits (e.g. £100,000 maximum balance and card purchase limits £10,000 per day and £20,000 per month)

Tide

The UK is one of the most popular jurisdictions for location-independent businesses due to several factors such as a stellar reputation, good access to services such as merchant accounts, and a good business environment.

The only significant obstacle for location-independent UK businesses with non-resident owners/directors was to open a bank account. No UK banks wanted to work with non-residents (unless you were bringing loads of business to the bank).

That was the situation until 2016.

Enter Tide.

Finally, there was a banking solution available to non-residents with UK registered companies!

Not only that, Tide also comes with automatic transaction categorization, accounting integration, multiple accounts, easy invoicing, and fully featured mobile and web apps.

You can choose from a free account (although transfers are 20p each), a Tide Smart account for £12.49 monthly (with 25 free transfers per month), a Tide Pro account for £24.99 per month (unlimited transfers), or a Tide Max account for £69.99 a month—which comes with highest level of support and 0.5% cashback.

Tide at a glance

Highlights

-

Unlike most UK banks, they accept UK companies with foreign directors/owners living abroad

-

You will get local GBP account details

-

Reasonable prices, powerful business features and apps

-

No currency exchange markup (you get the official Mastercard rate) with paid plans

Things to note

-

Supports directors of UK limited companies, regardless of residence, though a UK phone number/address is required. Sole traders, however, must live in the UK.

-

FX fee 2.75% with free plan

-

Tide does not currently support international bank transfers. However, you can use Wise for that.

-

Debit card limits of £25,000/mo for sole traders and £70,000/mo for limited companies

Honorable mention: Starling Bank

I would like to quickly mention Starling Bank while discussing banks for UK companies ![]() . It’s a great option, if both you and the business are resident in the UK. It’s not open to non-UK residents. The account has no monthly fee and lets you spend and withdraw cash abroad without Starling fees. If you want more advanced accounting features you can add the Business Toolkit onto your free business or sole trader account for £7 per month, the first month is free.

. It’s a great option, if both you and the business are resident in the UK. It’s not open to non-UK residents. The account has no monthly fee and lets you spend and withdraw cash abroad without Starling fees. If you want more advanced accounting features you can add the Business Toolkit onto your free business or sole trader account for £7 per month, the first month is free.

They also support Euro business account (£2/month) or a USD business account (£5/month). EUR/USD payments are free; internal GBP↔EUR/USD conversions are 0.4%.

If you qualify, definitely check it out.

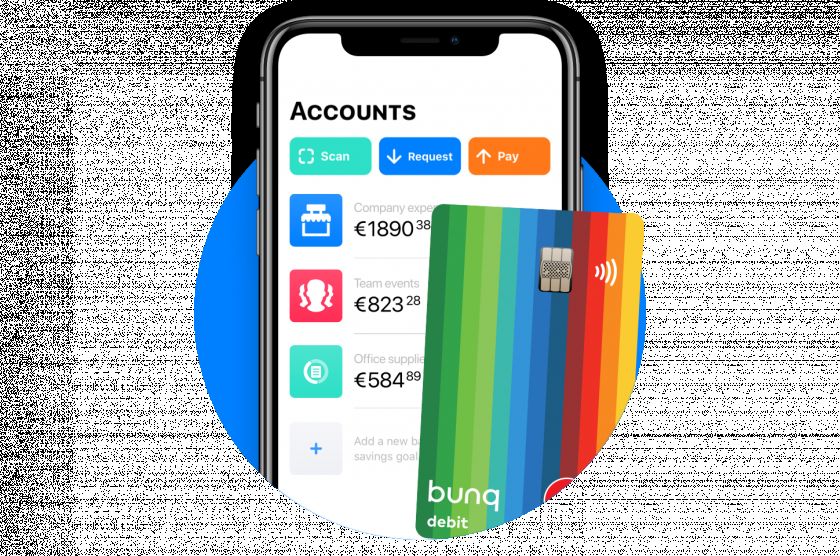

Bunq Business

Bunq is another bank that’s probably more known for their excellent personal accounts. But if you run a business based in the Netherlands, Germany, Spain, Belgium, France, Austria, Italy, Ireland or Portugal and reside in the same country then Bunq’s business account may be what you’re looking for.

It offers accounting integrations with many accounting systems. And in case there’s not direct accounting connection you can request automatic monthly CSV exports to send to your accountant or upload to your own accounting software.

Bunq Business comes with loads of other useful features, like multiple bank accounts, access for multiple users (to the whole account or just parts of it), and automatically setting aside VAT for your incoming payments so you’ll never come up short come tax day.

Bunq also strives to be an ethical bank, with responsible investment policies and you can even take control over where your money is invested (Freedom of Choice).

Bunq Business at a glance

Highlights

-

IBAN from the Netherlands, Germany, Spain, France, or Ireland

-

Popular bank in the Netherlands, which also offers corporate accounts in

:pt:

:pt:

-

Plans start from €3.99/month, they also offer a free option of basic features

-

They come with useful features such as auto-VAT management (for more premium plans), and automatic completion of payment details of scanned or PDF invoices

-

Powerful API so if you're technical you can automate a lot of your banking

-

Daily card spending limits of up to €50,000 which is among the highest limits I've seen when doing research for this article

-

0.75% interest in EUR, and 2.30% on USD/GBP with weekly payouts

Things to note

-

Free Business is for sole proprietors only (no employees/cards included by default)

-

Outgoing and incoming transfers are not free

Paysera

While it wouldn’t be my first option, Paysera is still a viable option if your business needs an EUR account and does not qualify for any of the options above.

They claim to support over 180 countries, however, unless you are in Europe—which seems to be mostly fine—the level of support may be limited. For example, registration and onboarding for clients in many countries outside of Europe have stricter requirements. Also onboarding is currently unavailable for citizens of many countries that they claim to cover.

Paysera at a glance

Highlights

-

Reasonably priced e-money account, based in Lithuania

-

Claims to support over 180 countries

Things to note

-

Transaction costs are not the lowest I've seen

-

Sometimes the recipient sees “Paysera” or intermediary info depending on bank/recipient country

-

Daily debit card limit of €10,000

Asia

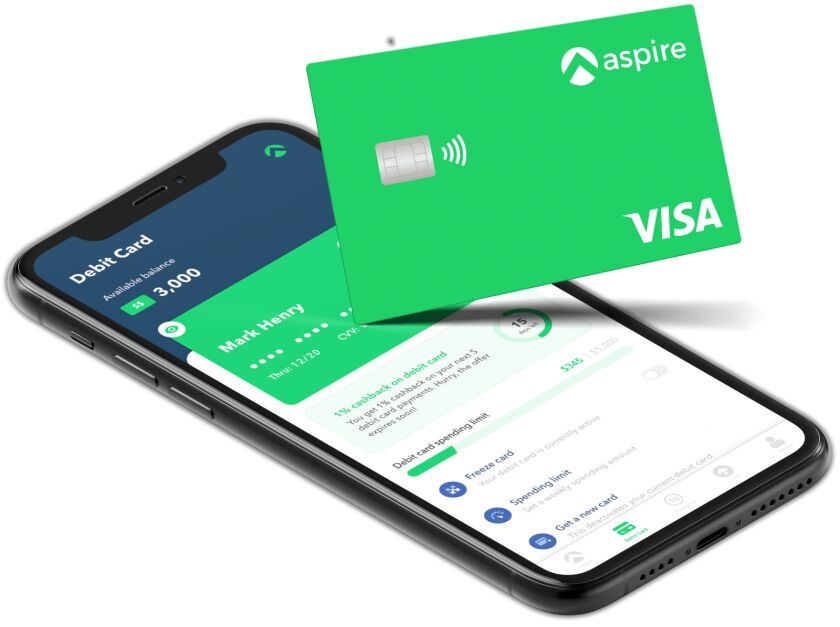

Aspire

TKTK: https://help.aspireapp.com/en/articles/9239713-what-countries-does-aspire-support

Singapore has one of the most favorable jurisdictions for businesses in Asia and very popular for location-independent entrepreneurs. While it’s usually possible to open business bank accounts with several Singaporean banks for non-resident owners, it typically requires in-person visits, a ton of paperwork, large minimum deposits, and often high charges for both account maintenance and transfers. So it’s no wonder that in 2019 Aspire was voted the number one hottest startup by Singapore Business Review.

You can open a business account with Aspire online in 10 minutes, but approval and activation of the account may take up to 5 business days. The account itself is free to open, there are no monthly fees, and no minimum deposit. Currently, you can open SGD, USD, EUR, GBP, and IDR accounts with them.

The free monthly account comes with two admin/finance accounts and 10 employee user accounts, as well as one physical card and unlimited virtual cards. Additional admin accounts are 9 SGD per user, and employee accounts 5 SGD per user.

It offers cheap international transfers at the mid-market rate, easy accounting, and 1% cash-back for some business costs. Also, you can apply for a line of credit easily in your Aspire account. Their convenient expense management system allows you to have a separate bank card for each employee with their own name and specified spending limits.

Aspire accepts clients with businesses incorporated in 16 countries but is primarily focused on businesses incorporated in Singapore.

Aspire at a glance

Highlights

-

Offers currency accounts in SGD, USD, EUR, and GBP

-

Can send and receive money in 30+ currencies across 130+ countries

-

Great FX rates

-

Accepts Singaporean and Indonesian companies, [as well a few others in the Asia-Pacific region](https://support.aspireapp.com/faq/what-countries-does-aspire-support), open to both local and foreign directors

-

1% cash-back with the card (on online marketing and Saas spend)

-

Offers yield on savings in USD (up to 4.38%) and SGD (2.54%)

-

Integrates with Xero and Wise

-

Offers incorporation options, if you also want to register a business with their help

-

Can apply for a line of credit up to S$150K

Things to note

-

Onboarding times are usually multiple business days (5-7)

-

Unclear fees for customers with businesses incorporated outside of Singapore

-

Some features (cards, receiving certain currencies, etc.) are not available to all business entities, especially those incorporated outside Singapore or Hong Kong

Other banks and regions

Most of the banks listed so far in this article are so called fintechs or neo banks. They work great for many types of businesses, but sometimes you may have more specific needs, or require services not offered by this type of bank.

Maybe you require an account in a specific country, or your business is incorporated in a jurisdiction that most banks won’t open accounts for? Or perhaps your business is classified as “high risk” by most banks?

If this is the case, you may want to open an account with a more established bank, or one that’s willing to work with more “high risk” clients. While this isn’t always straightforward, it’s more than doable if you’re armed with the right information.

I’d recommend that you stay away from so-called “bank introducers” that often charge thousands of dollars to introduce you to banks that would have accepted you anyway if you had applied directly. They don’t add much, if any, value.

Instead, I’d recommend asking people in your network who have successfully opened the type of account you’re looking for. Or if you don’t know anyone you can ask, I’d recommend signing up for a service like GlobalBanks.

They maintain a database of hundreds of banks in 50+ countries, including information about account opening requirements, fee schedules, reviews, tips for applying, including contact persons at many of the banks, whether you can open remotely, and so on.

Let me know in the comments if you know any other good options, or if you have any feedback about any of the ones I listed above!

Join  now!

now!

Get free access to our community & exclusive content.

Don't worry, I won't spam you. You'll select your newsletter preference in the next step. Privacy policy.