Note: This post is several years old and the below information may be out of date!

I have long been a fan of Wise, the startup that is taking the pain (and costs) out of cross-border money transfers. As a digital nomad, I need to transfer money around the world a lot, both to my own accounts and to other people. And I have used Wise to send money from Norway to both the US and Denmark, and most recently from Denmark to Germany.

Sending moderate sums of money from Norway to the US definitely saved me a lot of money. But this is largely due to the archaic banking system in the US (which is not part of SEPA, nor uses IBAN account numbers) and the complexity of international transfers outside of networks like SEPA. A regular bank transfer will usually incur a less than optimal exchange rate, and fees both with the sending and receiving bank, and often also with random banks along the way.

Sending money as a SWIFT transfer from my Norwegian account to an account in a San Francisco credit union incurred about $8 of fees in my Norwegian bank, $30 from some intermediary bank in New York and a $15 fee in the receiving Credit Union or their partner bank. So more than $50 in fees, and that’s even before you take into account that the bank is not giving me the mid-market exchange rate. Hence, Wise’s solution is quite attractive, with a flat 0.5% fee on top of the mid-market rate (and no fees with the sending or receiving banks). For large sums of money, this fee can become more expensive than the aggregate bank fees (if the exchange rate markup is less than 0.5%). But for small to mid-sized transfers, Wise is a godsend. It’s both cheaper and significantly faster.

But is that also the case within Europe? I designed a small experiment to find out, and the results will probably surprise you.

The experiment

I recently opened a euro account in Germany to test out N26 Bank, a new European banking startup with 100% fee free banking. Before instinctively transferring via Wise, I decided to check what it would cost to send the payment through my Danish bank. I was surprised to see that the rate shown in my Danish online bank was almost exactly the same as when I searched for the mid-market rate on Google. My Danish Bank has a DKK 20 (Danish Kroner, ~€2.68) fee when transferring money abroad, which is quite typical for the Danish market. As the transfer is effectively a SEPA payment in euros the receiving bank will not charge any fees.

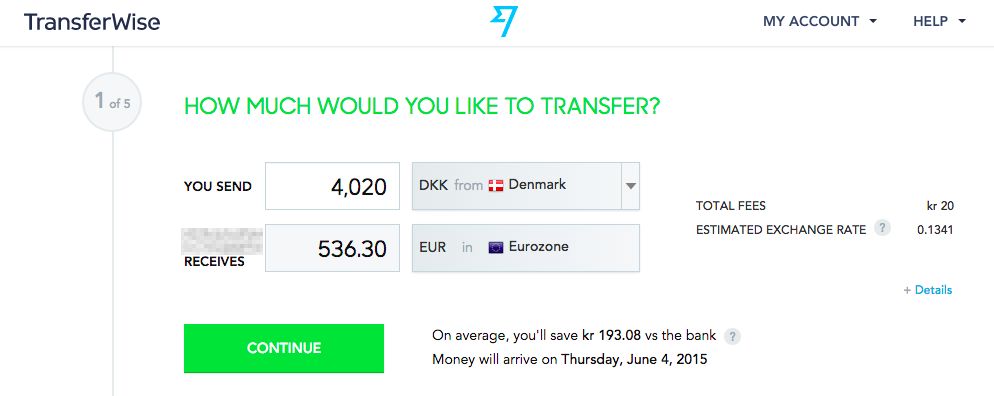

On paper, that means that if the size of the transfer is more than DKK 4000 (EUR 536.30) excluding fees, the cost will be the same for my bank and Wise. For larger transfers, my Bank will actually be cheaper. Yet, Wise is claiming to “most likely” be saving me more than EUR 25 on that specific transfer compared to my bank.

The set-up

-

I transferred DKK 4000 (excluding fees) to my new N26 account, both through Wise and directly from my Danish bank.

-

Because Wise asks me to denominate my transfer in DKK and my bank asks me to denominate the transfer in EUR, I decided to first set up the transfer in Wise, as it then told me approximately how much I would receive in EUR.

-

I then requested my bank to transfer the same amount of EUR as Wise estimated I would receive through them.

Since Wise charges a 0.5% fee on top of the mid-market exchange rate (which for DKK 4000 would amount to DKK 20 — the same as what my bank charges as a fixed fee), I set up a transfer of DKK 4020.

Since Wise estimated that I would receive €536.30, that’s what I requested my bank to transfer. The estimated cost of the transfer was DKK 4000.64 (this excludes the DKK 20 fee they charge for all outgoing SEPA transfers).

Basically, Wise estimated that I would get €536.30 for DKK 4020, and my bank estimated that €536.30 would cost me DKK 4020.64. But what would the actual result be?

What about speed?

I sent both transfers within a couple minutes of each other at approximately 10.30AM local time on Monday, June 1. This is well before the 1.30PM SEPA cut-off for effectuating transfers on the same day.

Originally, the way Wise worked was that you would transfer money to their local bank account in your country, and they would transfer the money to the recipient from a local bank account in the recipient’s country (or the same payment area, in the case of SEPA countries using EUR). That would put them at a disadvantage for SEPA transfers, as you would need to wait for first a local transfer, then a SEPA transfer to the recipient. If the local transfer takes a day to clear, the money would theoretically arrive a day later than if you transferred directly from bank to bank using a SEPA transfer. (Note, outside of SEPA, as in the case of transferring to/from the US, Wise would still be a lot faster than international bank to bank transfers.)

But now, Wise has added a debit card option (similar to Square Cash payments in the US, where the transfer amount is charged to your debit card instead of using a bank transfer).

This makes the payment from my bank to Wise instantaneous, and hence the total transfer period should theoretically be the same. Note that the “Estimated arrival” that was June 4 when I set up the transfer, changed to June 3 after paying with a debit card rather than a bank transfer.

The results

First, let’s look at the actual result of the currency conversions.

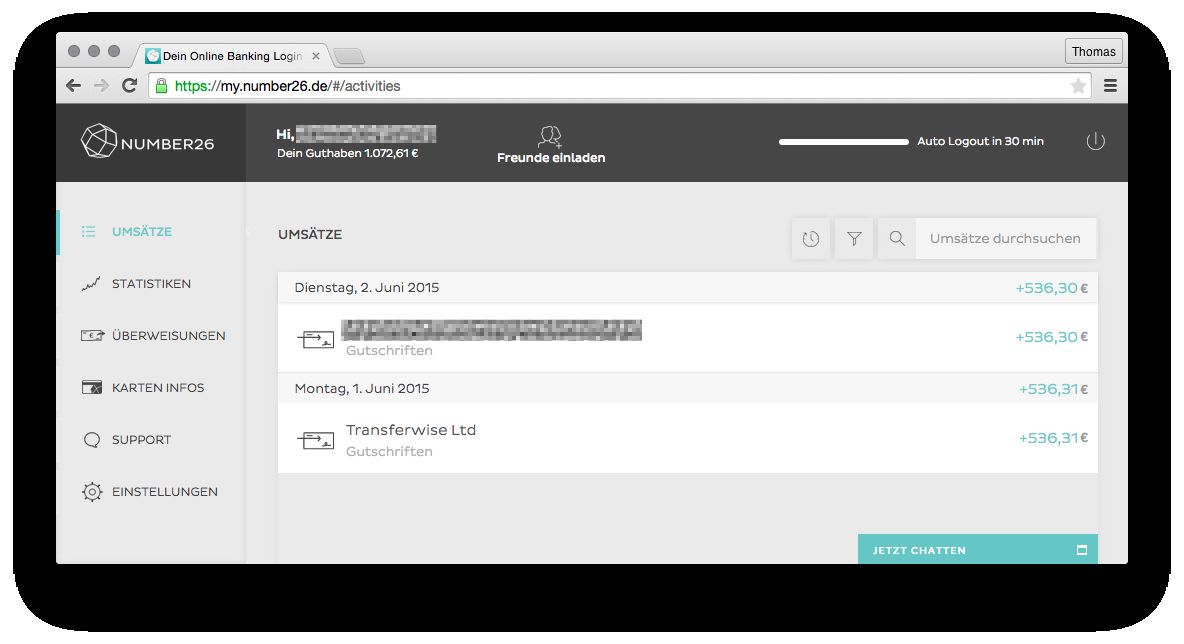

Less than an hour after initiating the transfers, both Wise and my bank had converted the DKK into EUR. Wise had estimated that my DKK 4000 would be converted into €536.30, which was very close to the truth. I ended up receiving €536.31, so an insignificant 1 cent gain.

DKK is actually pegged to the EUR at approximately DKK 7.46 per EUR, plus/minus a couple percent (not percentage points). This is good as the exchange rate has very small fluctuations, making it easier to estimate what markup the bank actually charges on the currency conversion.

My bank had estimated that my transfer of €536.30 would cost DKK 4000.64 (excluding the DKK 20 fee). The actually conversion resulted in a cost of DKK 4007.61, meaning that the bank to bank transfer was a mere €1 more expensive than through Wise. This means that the markup charged by my bank for the currency exchange is around 0.19%, which less than the 0.5% variable fee that Wise charges.

Armed with that information, it becomes quite straightforward to calculate when to use Wise and when to use my bank. Wise simply charges a 0.50% variable fee, while my bank charges DKK 20 fixed and 0.19% variable. So as long as 0.31% of the transfer amount equals less than the DKK 20 bank fee, Wise is cheaper. If we say that X is the transfer amount where my bank and Wise would cost the same, we only need to solve this simple equation:

0.0031X = DKK 20

X = DKK 20/0.0031 = DKK 6451.61

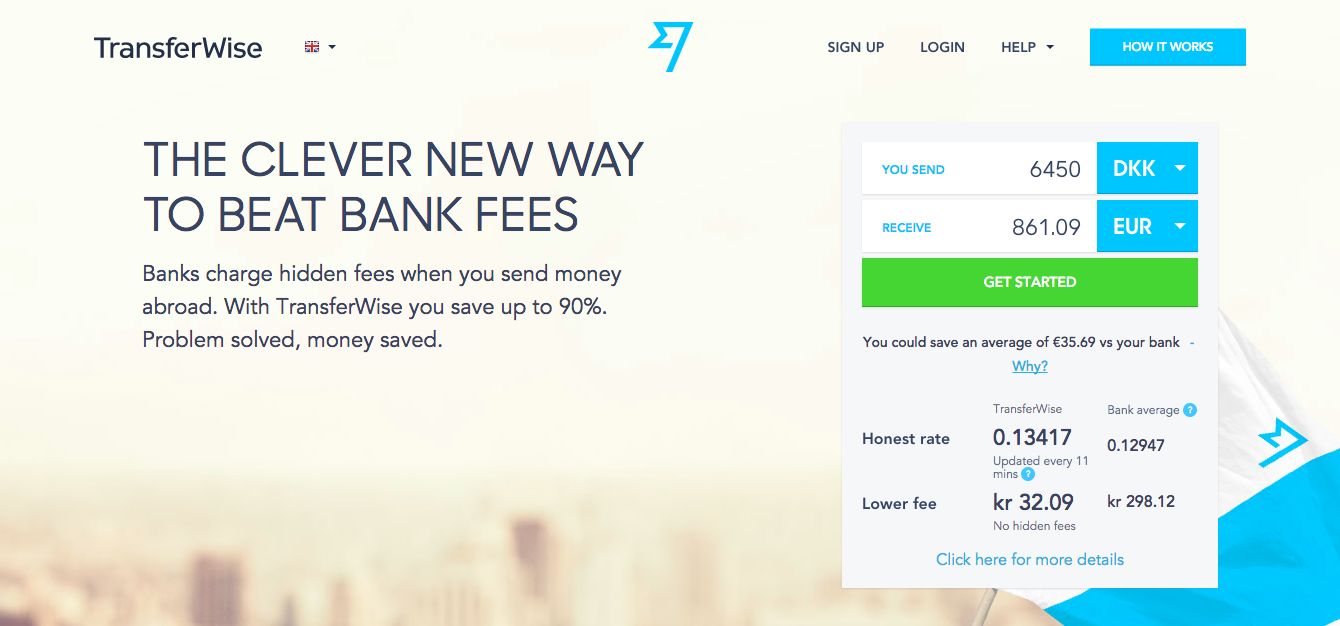

So there you have it! For transfers of more than DKK ~6450 (~€865), Wise is actually more expensive than my bank. Yet, Wise will proudly proclaim on their front page that such a transfer would save me over €35.

The estimate they provide is based on the costs of transferring GBP 1000 to EUR with a bunch of high-end (read: expensive) UK banks in November of 2014. Maybe it’s the case that UK banks are ridiculously expensive compared to my mid-sized, definitely average Danish bank. But if that is the case, it is extremely misleading for Wise to use very limited UK data to extrapolate estimates for other currency pairs. If they are displaying an average bank exchange rate for DKK/EUR, it better be based on actual data for that currency pair, with Danish banks.

Although I’m still a fan of Wise and will continue to use them when it makes sense, that’s just not cool business practices, and IMHO makes them just as manipulative as the banks they are trying to compete with.

While Wise has a “cheapest money transfer” guarantee, it really isn’t worth much when you have no way of proving what exchange rate your bank would have charged.

UPDATE: I reached out to Wise for a comment on my results and received the following statement from Antonia:

We’re committed to being transparent about our fees and savings to our customers. We’ve just completed price comparison research for DKK to EUR transactions and our fees calculator for Danish transfers will be updated in the very near future. While costs differ from bank to bank, the research we carried out this month showed that on average Danish banks charge 1.44% of DKK 7470 sent (approximately EUR 1000). Just like your test transaction showed, we found that Danish banks charge an average exchange rate mark-up of 0.17% and a fixed fee of DKK 20. We also found that customers may be charged other “hidden fees” that add to the costs of sending money abroad. For example, these can include receiving fees on the recipient’s end. Additionally we carried out a test transaction from DKK to GBP and found unidentifiable hidden fees that amounted up to DKK 60.88 for sending DKK 7470 abroad.

I’m glad to see that their findings were similar to mine. It’s worth noting that the “hidden fees” and the 1.44% average cost they refer to in the statement were experienced when transferring to other currencies than euro through SEPA. In fact with SEPA payments no hidden charges or fees are allowed. And Wise themselves use a bank account in Estonia to deposit money into all euro accounts in the SEPA area, so if your bank would charge you fees for receiving SEPA payments in EUR (they should not), the same fees would apply when Wise deposit the money.

Transfer speed

When it comes to speed, Wise ended up being faster. The money arrived already the same afternoon, which is pretty darn impressive. The bank to bank transfer arrived the next morning, around 10 AM, which is also pretty decent.

Conclusion

It is still clear that Wise is great for non-SEPA payments. SEPA payments not involving euros can still be cheaper through Wise than through many banks. But for SEPA payments too and from euros I would recommend checking your bank’s fixed fee and exchange rate markup – thanks to SEPA rules it might be even cheaper than Wise, especially for larger payments.

Check out Wise now or read more about it on Nomad Gate.

For more tips, resources and news for frequent travelers, nomads, and other location-independent professionals, sign up for Nomad Gate.

SEPA countries with euro: Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Portugal, Slovakia, Slovenia, Spain, Monaco, San Marino, and Andorra.

SEPA countries with other currencies: Bulgaria, Croatia, the Czech Republic, Denmark, Hungary, Poland, Romania, Sweden, United Kingdom (for now), Iceland, Liechtenstein, Norway, and Switzerland.

Note: Some links in this article are referral links, in accordance with this policy.

Join  now!

now!

Get free access to our community & exclusive content.

Don't worry, I won't spam you. You'll select your newsletter preference in the next step. Privacy policy.